Here we are heading into 2026, and with medical insurance, the one constant over the last 10 years has been said, reported in the news, and generally complained about: the increasing costs of medical insurance. The last 12 to 18 months have seen the largest premium increases in 30 years!

As an advice business, we need to adapt to a significantly more challenging market. Here's how we are responding.

In the last 20 years, and more acutely in the last 5, relying on the public health system's response has become more difficult than improved. On top of that, we now have a significant number of critical medicines and treatments that are not funded.

We are now in a time when access to health care is harder, and it comes with significant costs, meaning medical insurance isn't the nice-to-have it might have been 20 years ago. It is now essential to both your survival and the protection of your lifestyle.

We continue to see people dropping their medical cover in a knee-jerk reaction of "It's too expensive" without considering that reducing coverage to fit your budget will still protect you from the really big stuff you need coverage for.

Someone who has been paying $600 per month for coverage and now it's $800 isn't complaining they don't have the $600 to keep going; they're complaining they don't have the $800 to keep going as it was. Keeping that spend at $600 per month (or lower as needed) will still provide a reasonable level of coverage when we sit down and have a chat about it.

Sure, we get it, you've paid premiums for decades, and it's been relentless with increased costs. I'm going to show you how relentless it is in a second. Comments often include statements about loyalty and being a good customer that go unrecognised.

Hold up. That recognition of loyalty isn't what you think it is to the insurer. More to the point, as a policyholder for decades, you now represent one of the insurer's biggest risks for large claims. When routine treatment of Breast Cancer costs $100,000 without fancy medicines, we are talking big numbers.

Where am I going with this?

It's tough out there; we hear about it every day. At the same time, you really don't want to be at the mercy of the public system when you have paid for medical insurance this long, and public health is at its lowest point.

Take a breath and let's talk about restructuring what you have so it best suits you for the budget you have.

The reality is that the type and structure of your medical policy should change over time, both because it is too damn expensive and because different stages of life require different approaches.

Most people look at medical insurance, basing their decisions on the idea that the policy will remain untouched and unchanged for 40-plus years. That is blatantly unrealistic.

What I want to outline for you is the possible life cycle of someone's cover and its cost based on today's premiums.

Let's get started:

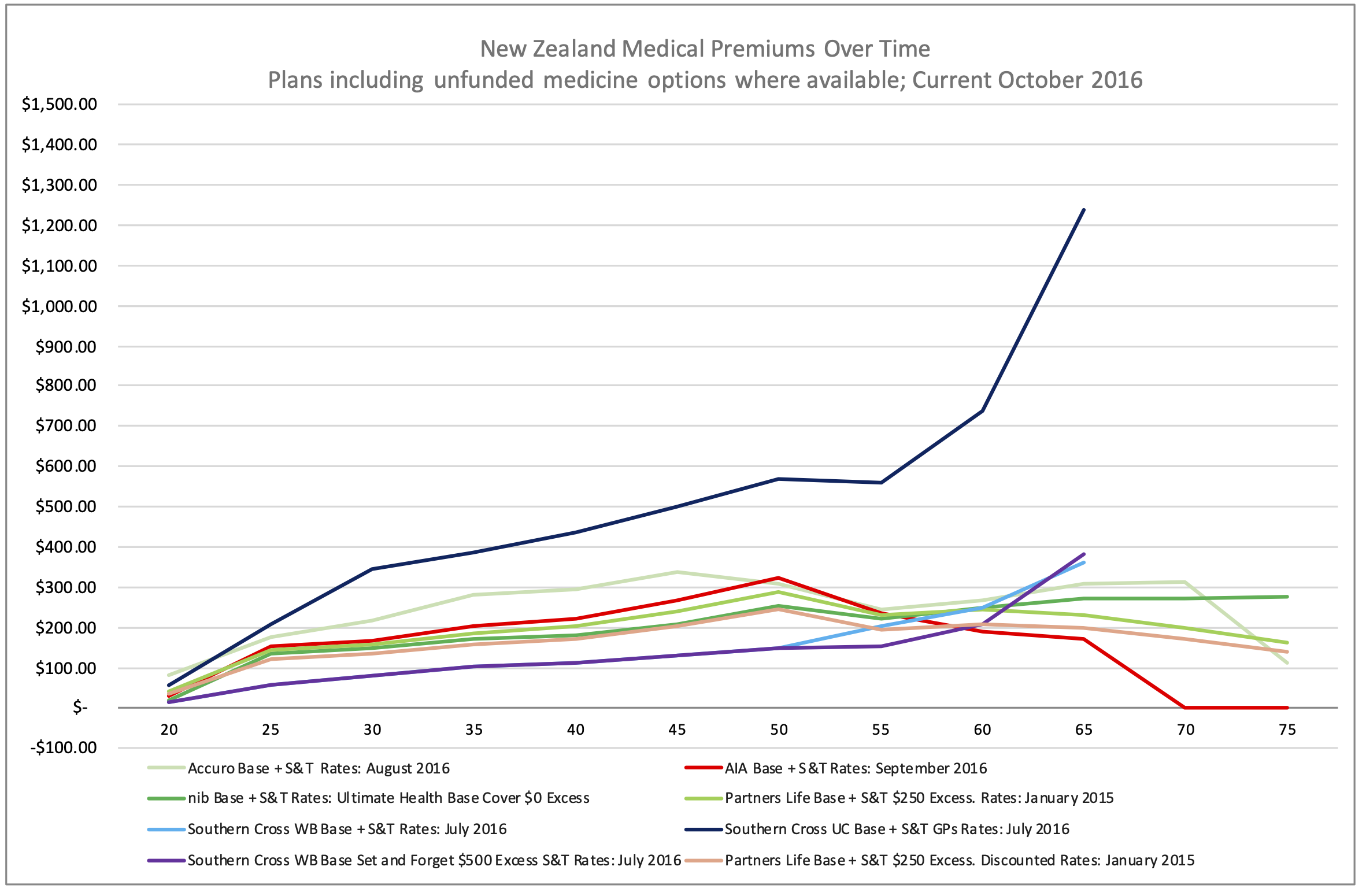

For context, I'm going to start with the following: this is what premiums looked like in 2016. I've gone back to the original data from my previous series and recreated what today's advice would look like with the 2016 premiums. Somewhat scary stuff, but also some perspective on how premiums have climbed over time, which is also a long-term consideration.

- Also, keep in mind the changes in your own situation and income during that time frame.

- The reality of these premium increases is the tipping point that has been reached only in the last 12-18 months.

I'm going to talk through the various stages medical cover goes through and some of the decisions that get made. But first the contrast.

This is what 2016 premiums would look like with the policy lifecycle I'm going to outline. (Over age 65 there is limited data)

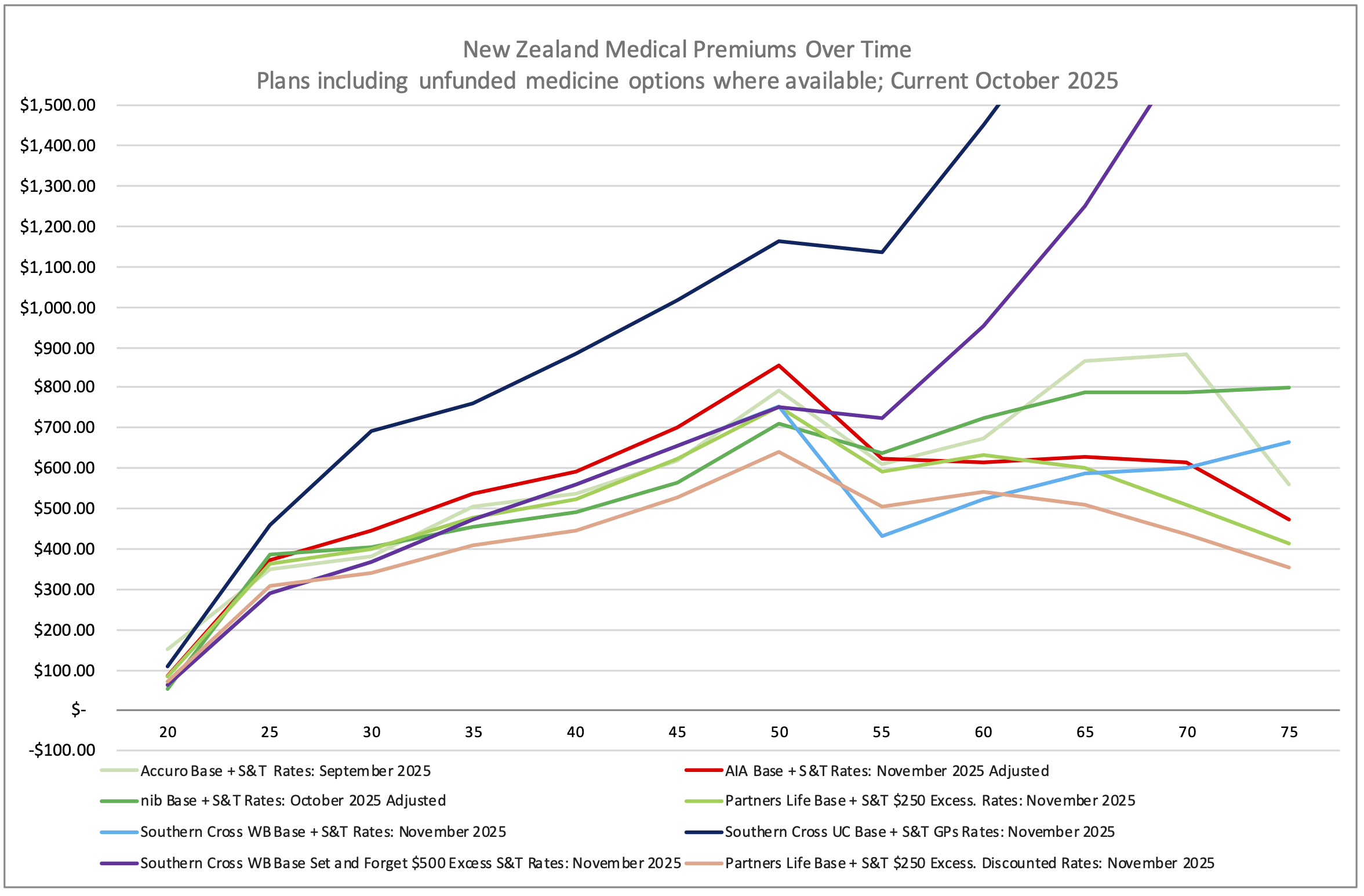

A time when $300 per month for medical premiums was expensive. Today, the picture is a bit different. This is October 2025.

Premium is accurate at the time of publishing, based on standard premium rates and subject to a medical assessment. Discount premiums require additional policy benefits to access that may or may not be appropriate for an individual situation. Some providers have additional plans available; the most equivalent plans have been used for comparison purposes.

When we have this magnitude of change from a 50-year-old having a $300 premium to now being more like $700, something has to give. People's incomes haven't risen as fast as medical premiums have.

The stage is set, let's get started on the runway.

20:

Ok, you’re 20, and you probably have medical insurance from your parents, though you may have arranged it yourself. The most likely scenario is that you have it from your parents’ plan, and they’re probably still paying for it. The average premium at this stage for a hospital plan with specialists & tests and a $250 excess is about $70 per month, or around $2 per day.

25:

Roll on a few years, and you’re 25, partner on the scene, and you’re clear of the children's premium rates that you may have been on when you were 20. Cover needs haven’t changed, though adult premiums have affected the monthly premium: it's now $344 for both of you.

30:

30 rolls around, and there’ve been a few changes; married and a baby, things have changed quite quickly. The average age of a bride in NZ is 28.5 years, and the groom is 30 years old. With Mum for the first time at about age 30. With the addition of bubs, your premiums have increased a bit to $390 per month on average. At this stage, the excess is moved to $500 to help accommodate the added cost of bubs.

35:

A few years later, at age 35, number two is on the scene, and the first one is off to school; you need the type of cover you had, and the premiums are now approaching $475 per month.

40:

40 rolls up and hits you from behind. The kids are well into school, and there have been a few specialists and tests claims, and one of you may have had surgery. Things are starting to show up, and your cover is now returning some of that value you’ve really wanted to avoid. Premiums haven’t changed significantly, averaging $523 per month. If you were to take cover now, you’d face exclusions for pre-existing conditions, which also means moving between providers would have a similar issue.

45:

45 whistles up, and the kids are in high school; there may be some additional resources available to increase the excess. At this stage, it’s not going to make much difference, and there’s a test pending, so we leave it be. Average premiums have been slowly creeping up; it’s now approaching $615 per month.

50:

50 comes around faster than you'd like; you still feel like you’re 30. So why are the premiums getting so high, around $750 per month? The kids are at Uni and soon to be off your hands, though not as soon as you may like. Some providers are starting to charge an adult premium for the kids. We leave it be as the kids will come off soon, and that will help.

55:

55 now, we need to get serious about the retirement plan. This medical insurance premium needs to be better managed. We’ve dropped the kids off on their own policies, and with specialist and testing premiums being around $250 per month as a couple, it's time to consider self-insuring for the minor things. At $250 per month, unless you're regularly seeing a specialist, it doesn't make much financial sense. We do need to be mindful of major tests, and these should still be available under major diagnostics without requiring hospitalisation. (Southern Cross only enables endoscopies at this stage) We drop off specialists and testing, and keep the excess at $500; this brings the average premium back under $600 per month, to $565.

60:

60 arrives, you’ve had a serious claim, and there are a few medical things going on; we need to retain the cover but ensure it does a good job when it's needed. There’s the occasional big test, but this is manageable, so we plan to increase the excess to $1,000 at this review. The average premium comes back to $618 per month. Specialists and testing are claimable with a surgery admission, provided they are within 6 months of the admission date.

65:

At retirement, and at age 65, the key focus is substantially reducing costs as income declines. This is where we make a tough decision, increase the excess to $2,000. This change means a substantial part of your cover for major diagnostics will now be at your own cost. The average premium comes back to $663 per month with this approach.

70:

70 comes around much faster than you wanted, and premiums have been creeping up too. Retirement savings and plans have gone better than expected; we look at increasing the excess to $4,000 to keep premiums affordable at $638 per month. The premium range at this point is $434 to $882 per month, depending on the provider. (Excluding Southern Cross UltraCare at $2,221)

75:

At age 75, we push the excess out as far as we can. For some providers, that was done at the age 70 review; for others, we offer a $10,000 excess option. This means the really serious things will still be covered; anything minor is likely to be at your cost. Financially, things haven’t been too bad, and premiums are now in the $351-$799 range for both of you. About what things were costing back at age 30, but with a significantly reduced policy response.

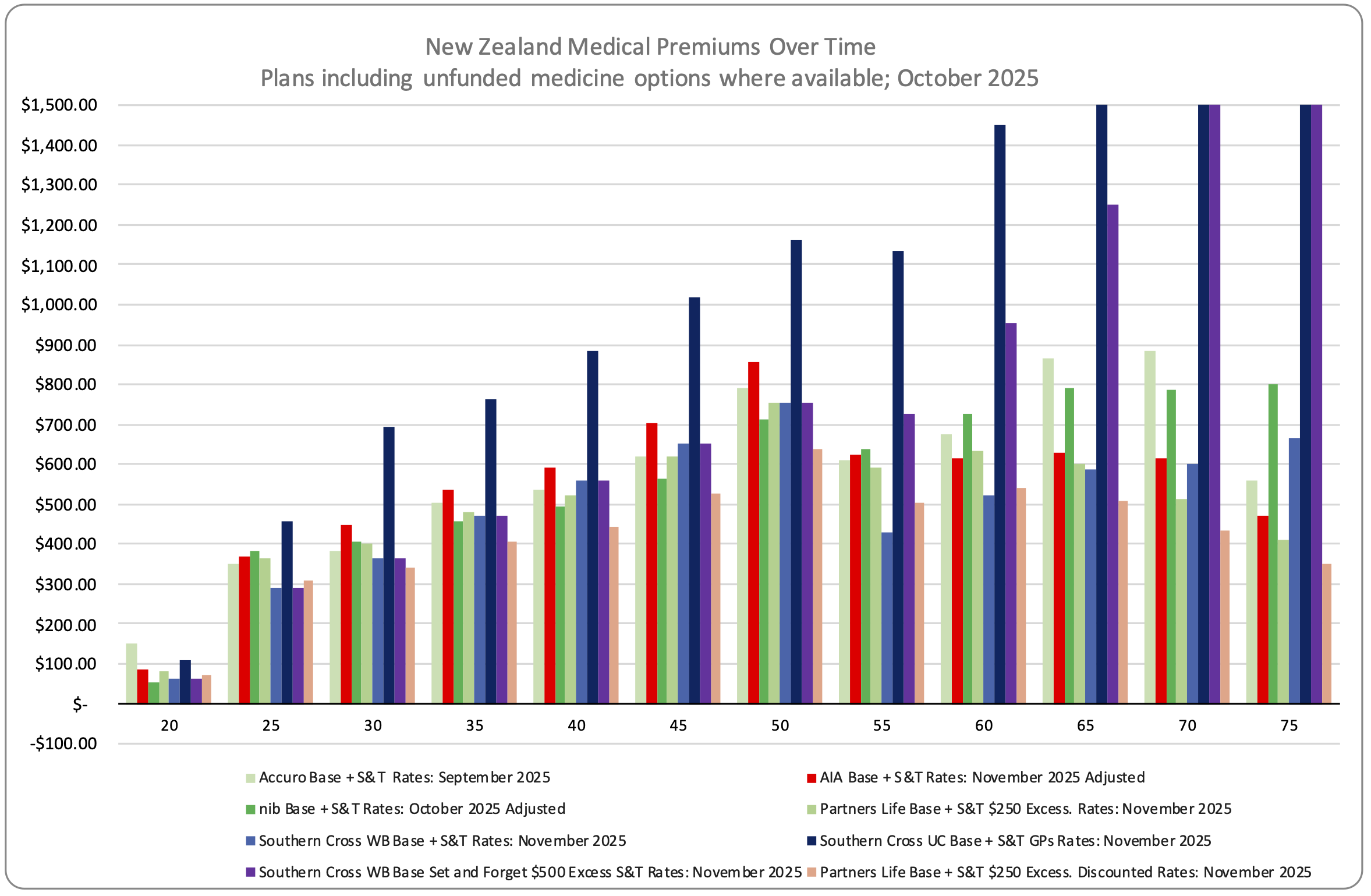

The graph below covers the same information as above, but provides a clearer view of what each provider is doing at a given age.

Premium is accurate at the time of publishing, based on standard premium rates and subject to a medical assessment. Discount premiums require additional policy benefits to access that may or may not be appropriate for an individual situation. Some providers offer additional plans; the most comparable plans have been used for comparison purposes.

Summary:

Looking across all providers and ages for this typical scenario, the average premium is $574 per month. Some providers will be consistently positioned, while others will be across the spectrum, as age and policy structure have a greater impact than with other providers.

This is an outline of a typical medical insurance strategy and one that plays out every day. This isn't my advice at work; these are the decisions clients make once they have the information to make informed decisions that affect them. Being able to discuss the options means you retain valuable benefits that you may have otherwise cancelled because you saw no other option.

I’ve seen people with very few claims and others with multiple claims and thousands paid. For example, a couple of knees and a bypass, $85,000 within 3 years, and cancer surgery and treatment, $265,000. Sometimes it's nothing for years and years, then bang, it's a run of significant claims; other times it is a consistent run of more minor things, but they add up in the same way. Everyone is different; that's sort of part of my point.

These aren’t small numbers, and most New Zealand families would be hard-pressed to fund them. Your average medical policy provides $600,000 to $1,000,000 of coverage per person per year. With two saying, they are unlimited. The majority of people get nowhere near that in one year, let alone a lifetime, but it’s there if it’s needed.

If you take coverage at 30 for you and your family, hold it until age 75. As I’ve outlined, on average across all providers, you’ll pay about $310,150 in premiums, which is a reasonable chunk of money. Remember, this is over 45 years, and that’s a long time for trying to save this. $260,000 if we leave out UltraCare, which disappears into the stratosphere.

If you and your family have $10,000 in claims every year. Which is unlikely but possible, you’ll have an insurance payout of $450,000 straight off. If we look at average incomes over this period, they amount to just under 5% of gross income.

Imagine what our health system would look like if it had 5% extra funding from a direct tax! I probably wouldn't be having this chat with you, and I'd be talking about something else. Unfortunately, it's not going to change in a hurry; medical insurance is a significant need in society.

If you take the cheapest option in this group, which is still a good policy, you’ll be about $11,729 better off than the average. If you take the most expensive plan, you’ll be about $26,224 worse off than the average and still on a reasonable plan. (Excluding UltraCare)

Interestingly, the plan in the middle of the pack is the one with the least resources available to cover you in the future.

So is it worth it? Definitely!

Have a chat with us about how you can do this in a cost-effective way for you so you get the best treatment options available for your premium $ so that it’s affordable into the future for you and your family.

Terms & Conditions

Subscribe

My comments